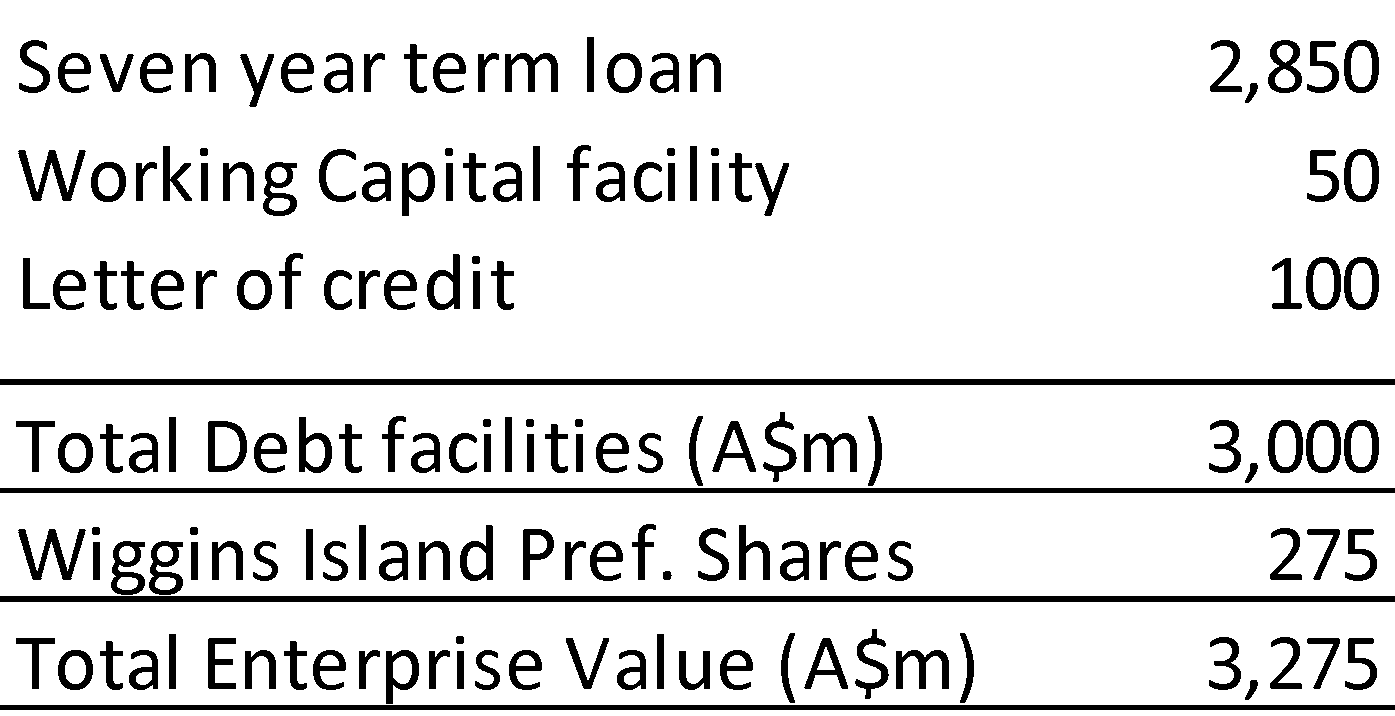

Australia & New Zealand Banking Group Ltd. (ANZ) and Westpac Banking Corp. (WBC) are among lenders risking losses on $3 billion of loans backing a coal port in Australia that will be twice its required size.

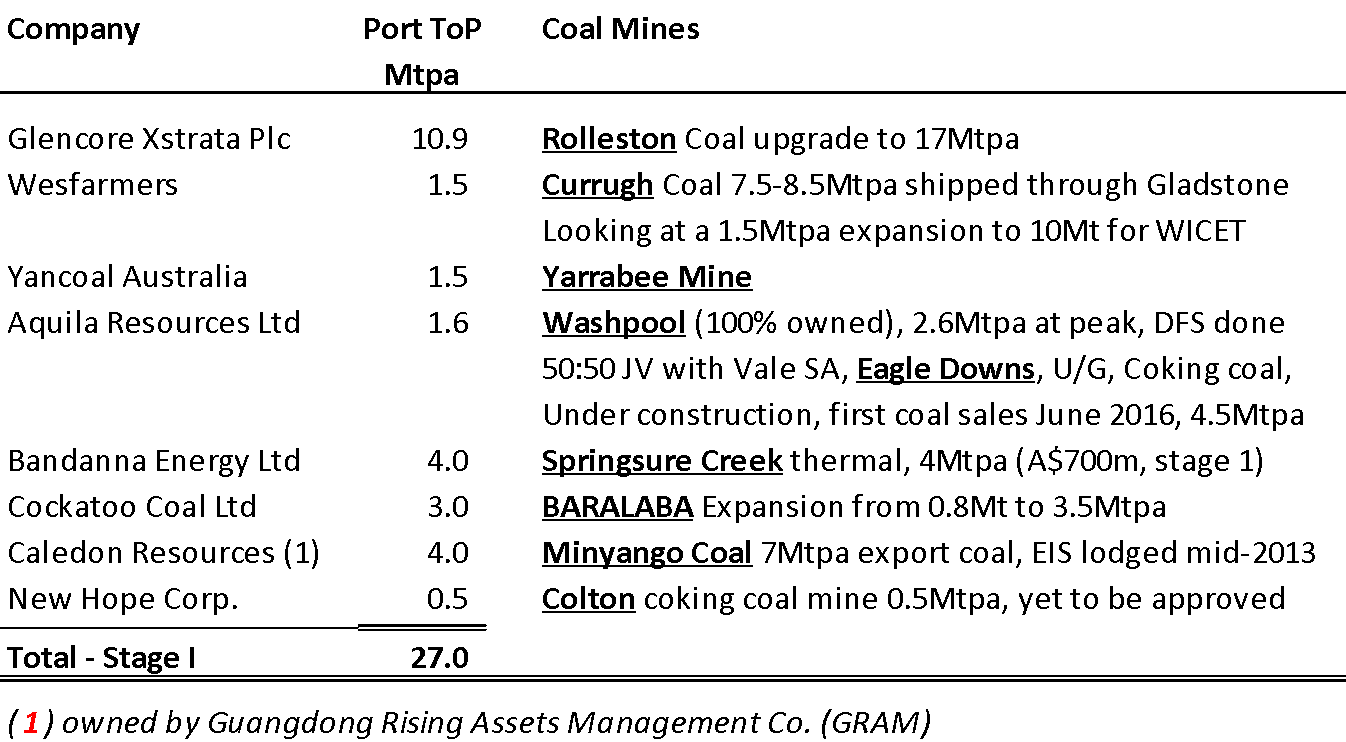

Wiggins Island Coal Export Terminal Pty, the group comprising the unfinished project’s owners, including Glencore Xstrata Plc (GLEN) and Wesfarmers Ltd. (WES), in 2011 borrowed the debt from 19 banks, according to data compiled by Bloomberg. When the port in the state of Queensland begins shipping in early 2015, only about half of its 27 million metric tons of initial annual export capacity will be used after a slump in coal demand, forecaster Wood Mackenzie Ltd. estimates.

“There will be more capacity than mines available to utilize it,” Daniel Morgan, a Sydney-based analyst at UBS AG said in a phone interview. “It may result in the banking syndicate having to renegotiate the terms or the price, or taking a writedown on their position.”

To secure the funding, Wiggins Island’s coal company owners committed to take-or-pay contracts, which oblige them to still pay for any of their unused export allocation. The junior owners may struggle to meet those contractual obligations after falling coal prices delayed new projects, said Morgan. The owners also had to provide bank guarantees that covered them for a year if they couldn’t make payment.

A load of coal is loaded onto a ship berthed at the Port of Newcastle in Australia. Companies are delaying new mines and expansions after a supply glut in power-station coal forced prices to a four-year low in August. Close

A load of coal is loaded onto a ship berthed at the Port of Newcastle in Australia.... Read More

A load of coal is loaded onto a ship berthed at the Port of Newcastle in Australia. Companies are delaying new mines and expansions after a supply glut in power-station coal forced prices to a four-year low in August.

Lloyds Exclusion

Westpac, one of the original lenders to Wiggins Island, excluded the project’s debt from a package of loans it bought from Lloyds Banking Group Plc last week, when it acquired its Australian assets, according to a person familiar with the matter. The Sydney-based lender didn’t want any more exposure to the project, that person said.

Glencore, the world’s biggest thermal coal exporter, is trying to sell 5 million tons of a contracted 10.9 million tons of Wiggins Island capacity to other users “due to changed market circumstances,” according to Francis de Rosa, a Sydney-based spokesman. It hasn’t received any offers, he said.

Spokesmen for Westpac, ANZ and Commonwealth Bank of Australia declined to comment on the loans and National Australia Bank Ltd. (NAB), wasn’t available to comment. All were included in the original syndicate, Bloomberg-compiled data show. Westpac wasn’t available to comment on the exclusion of Wiggins’s debt from the Lloyds purchase.

Alasdair Jeffrey, an external spokesman for the Wiggins Island project, wasn’t immediately able to comment on the port’s contract obligations, or Westpac’s exclusion, when contacted by phone.

Workers inspect a massive dragline bucket at the Curragh coal mine owned by Wesfarmers Ltd. in central Queensland, Australia. Close

Workers inspect a massive dragline bucket at the Curragh coal mine owned by Wesfarmers... Read More

Workers inspect a massive dragline bucket at the Curragh coal mine owned by Wesfarmers Ltd. in central Queensland, Australia.

Subordinated Debt

The Wiggins Island bank debt comprises a $2.85 billion seven-year term loan, a $50 million working capital facility and a $100 million letter of credit, Bloomberg-compiled data show. The letter of credit also has a seven-year maturity while the working capital loan is tied to the port’s completion date, expected in early 2014, the data show. The package included senior and subordinated debt arranged by ANZ, according to Wiggins’ website.

“The development has a complex capital structure which will present challenges if there are any issues in cost overruns,” said Chris Wyke, a Sydney-based managing director at financial adviser Moelis & Co. “It’s reportedly on track for completion, after which there are very real risks that some of the parties can’t meet their take-or-pay obligations.”

Aquila, Bandanna

More than 60 percent of the port’s first stage is already built, said Jeffrey. Its capacity has the potential to expand to 80 million tons over two more stages, he said. The port’s other owners are Yanzhou Coal Mining Co.’s Yancoal Australia Ltd., Aquila Resources Ltd. (AQA), Bandanna Energy Ltd. (BND), Cockatoo Coal Ltd. (COK), Guangdong Rising Assets Management Co. and New Hope Corp, according to Wiggins’ website.

“Over the opening years of the terminal, between 2015 and 2017, we’d expect capacity utilization between 40 percent and 60 percent,” Ben Willacy, Wood Mackenzie’s manager of coal cost research in Sydney, said by phone. “That’s a result primarily of projects that are due to be feeding Wiggins Island not being developed on the original time frame that was planned.”

Companies are delaying new mines and expansions after a supply glut in power-station coal forced prices to a four-year low in August. BHP Billiton Ltd. (BHP), the world’s biggest exporter of coking coal, last month flagged a “challenging” market for steel-making coal because of muted demand and oversupply.

Power station coal prices have declined 36 percent to $78.65 a ton since September 2011, when the Wiggins debt was finalized. Steel-making coal fell 47 percent to $147.75 a ton over that time frame, according to Energy Publishing Inc.

More Capacity

At Wesfarmers’ Curragh mine which currently ships through the Port of Gladstone, an expansion of capacity to 10 million tons annually from about 8.5 million tons “will be dependent upon market conditions,” according to its annual report. Kent Beasley, a spokesman for the company’s resources unit, declined to comment on the use of its 1.5 million-ton annual allocation at Wiggins Island.

“You’ve got a number of large coal companies in that first stage with established coal operations -- Glencore Xstrata, Wesfarmers and Yanzhou -- and those we anticipate will feed into stage one very easily,” Wood Mackenzie’s Willacy said. “But it will be harder to develop new greenfield projects in time for the start of the terminal.”

Bandanna and Guangdong Rising Assets Management plan to develop greenfield projects, he said.

Junior coal miners are struggling with reduced valuations in the “current atmosphere,” said UBS’s Morgan. “The ability to sell down a stake in their projects to help with finance is also problematic - it’s a buyers’ market.”

Potential Partners

A planned mid-2015 production start for Bandanna’s A$700 million ($662 million) Springsure Creek thermal coal project is subject to funding and government approvals, the company said last month. Bandanna, with a market value of A$95 million and about A$74 million in cash as of June 30, has sought potential partners since 2011. It’s contracted to pay Wiggins Island A$54 million annually, according to a May 1 Credit Suisse report, citing company data.

Bandanna last month delayed the start of rail services and related take-or-pay charges with coal haulage provider Asciano Ltd. from 2014 to 2016, according to a statement.

“The debt holders will likely have to share some pain and provide concessions,” said Paul McTaggart, a resources analyst at Credit Suisse Group AG in Sydney. “Putting coal juniors out of business would mean no coal at all and that’s certainly not what the debt providers would want.”

To contact the reporters on this story: Elisabeth Behrmann in Sydney at ebehrmann1@bloomberg.net; Paulina Duran in Sydney at pduran10@bloomberg.net

To contact the editor responsible for this story: Andrew Hobbs at ahobbs4@bloomberg.net